Vietnam soft drink industry

Vietnam is the fourth-largest economy within the Association of Southeast Asian Nations (ASEAN). Its total land area spans approximately 330,000 square kilometers, and as of 2023, its population was estimated to be around 103 million.

In recent years, Vietnam has experienced rapid economic growth and rising household incomes, which has led to an increased demand for soft drinks in the country. This surge in demand has been documented by CRI.

In 2023, the soft drink industry in Vietnam experienced significant growth, with total sales volume reaching 4.658 billion liters, representing a 4.8% increase compared to the previous year. According to the Consumer Research Institute (CRI), the market is primarily driven by three key segments: ready-to-drink tea, bottled water, and carbonated beverages.

Ready-to-drink tea emerged as the dominant category, accounting for 34.2% of total soft drink sales in 2023, with a volume of 1.594 billion liters. Bottled water witnessed the most remarkable growth, with a compound annual growth rate (CAGR) of 9.9%, resulting in sales reaching 940 million liters in 2023. The growth of carbonated beverages was comparatively modest, with annual sales reaching 824 million liters in 2023.

Factors Influencing Vietnam Soft Drink Industry

The Vietnamese soft drink industry is influenced by a confluence of factors. In 2023, Vietnam’s Gross Domestic Product (GDP) grew by 5.05%, falling short of the initial projection of 6.5%. To bolster businesses and consumers, the Vietnamese government reduced the value-added tax (VAT) rate from 10% to 8% from July 2023 to the end of the year, fostering the expansion of the fast-moving consumer goods sector, which includes soft drinks.

According to CRI, in addition to supportive government policies, the surge in outdoor activities and travel among Vietnamese citizens following the easing of COVID-19 restrictions has also fueled soft drink sales. With increased time spent on work, education, and leisure activities outside the home, demand for various products, including soft drinks, has escalated.

In terms of retail channels, e-commerce continues to increase its share in the distribution of soft drinks in Vietnam, benefiting from the rising internet penetration rate and the increasing variety of stores, apps, and platforms offering online sales. According to CRI, many Vietnamese soft drink brands are striving to open official stores on popular e-commerce platforms.

According to CRI, grocery stores remain an important sales channel for Vietnam’s soft drink market due to their convenient locations, especially in rural areas where other channels are limited. As for modern channels such as convenience stores, supermarkets, and hypermarkets, their share has been rising in recent years, supported by urbanization and the increasingly modern lifestyles of Vietnamese consumers.

In the Vietnamese soft drink market, Suntory PepsiCo Vietnam Beverage Co Ltd is the dominant player, holding a leading position in carbonated beverages, juice, bottled water, and sports drinks. This dominance makes it the largest soft drink company in Vietnam based on non-trade sales volume, according to CRI. Coca-Cola Beverages Vietnam Co Ltd is another significant participant, with a strong presence in carbonated drinks, bottled water, and juice. Tan Hiep Phat Group is a noteworthy local company, ranked second overall. Its tea beverage brand aligns well with current health and wellness trends, but it faces competition from other players in this segment, including URC Vietnam Co Ltd.

During the COVID-19 pandemic, Vietnamese consumers have prioritized health and wellness, a trend that has persisted since. Market research from CRI indicates that Vietnam’s soft drink market has seen a shift in preferences.

While sugary drinks remain popular in the summer months, healthier alternatives have gained significant traction. Categories such as reduced-sugar and sugar-free carbonated beverages and instant teas have witnessed substantial growth. Niche products like functional beverages and plant-based protein drinks have also experienced strong demand due to their perceived health benefits.

To address this growing consumer demand, many soft drink companies have introduced low-sugar or sugar-free variations of their established brands. They have also enhanced their products with added vitamins and minerals to appeal to the health-conscious market.

Sustainability is also a development trend in the industry, with more Vietnamese soft drink brands committing to using 100% recycled materials in their packaging. This drives the development of a circular economy in Vietnam, turning waste into resources rather than releasing it into the environment. Manufacturers are also working to encourage consumers to recycle bottles by displaying messages like “Recycle Me” on packaging to raise awareness and motivate people to take action.

CRI predicts that the performance of the soft drink industry will remain stable during the forecast period, with major market players continuously stimulating demand through new product development, active marketing campaigns, and special events.

CRI expects bottled water and juice to be the most dynamic categories in Vietnam’s soft drink industry in the coming years, benefiting from their healthier image. In contrast, the growth rate of carbonated drinks is expected to slow due to their increasingly unhealthy image and concerns about their high sugar content.

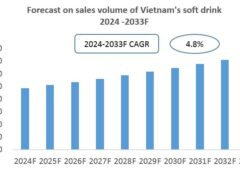

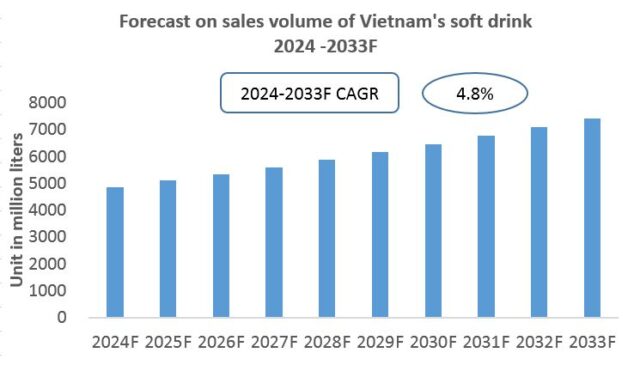

CRI predicts that the sales volume of Vietnam soft drink industry will reach 7.453 billion liters by 2033, with a compound annual growth rate (CAGR) of 4.8% from 2024 to 2033. Different types of soft drinks are expected to have varying growth rates.

CRI anticipates that beverage brand companies, beverage producers, and beverage distributors will find potential investment opportunities in Vietnam’s soft drink market. Packaging producers and other related companies in the beverage industry will also find many opportunities in the Vietnamese market.

Topics covered:

- Overview of Vietnam’s Soft Drinks Industry

- Economic Conditions and Policies for Vietnam’s Soft Drinks Industry

- How Foreign Investment Enters Vietnam’s Soft Drinks Market

- Market Size of Vietnam’s Soft Drinks Industry (2019-2023)

- Analysis of Major Soft Drinks Manufacturers in Vietnam

- Key Drivers and Market Opportunities in Vietnam’s Soft Drinks Industry

- What are the Main Drivers, Challenges, and Opportunities for Vietnam’s Soft Drinks Industry during the Forecast Period of 2024-2033?

- What is the Expected Revenue for Vietnam’s Soft Drinks Market during the Forecast Period of 2024-2033?

- What Strategies are Major Market Players Adopting to Increase Their Market Share in the Industry?

- Which Segment of the Vietnam Soft Drinks Market is Expected to Dominate by 2033?

- Forecast of Vietnam’s Soft Drinks Market (2024-2033)

- What are the Main Adverse Factors Facing Vietnam’s Soft Drinks Industry?

Full report: Vietnam Soft Drinks Industry Research Report 2024-2033